26/03/2012 21:48 26/03/2012 21:48 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Settore immobiliare

Corea del Sud, aziende alle prese con la flessione del real-estate

26 Marzo 2012

Woongjin Group, un conglomerato coreano di medie dimensioni, sta lanciando la vendita di una quota del 30% della propria impresa di depurazione, Woongjin Coway. Si tratta di un'operazione che riveste un ruolo rilevante non solo in termini monetari (varrà circa 2 miliardi di dollari). Ma anche – spiega il Wall Street Journal, che riporta la notizia – perché segnala gli effetti a catena della flessione dell'immobiliare sudcoreano.

I proventi, infatti, verranno utilizzati per rinforzare il bilancio del gruppo, messo in difficoltà soprattutto da soprattutto Kukdong Engineering & Construction, acquisita nel 2007. Si tratta di una società di costruzioni che (insieme alle due casse di risparmio assorbite dal gruppo nel 2010) è stata pesantemente colpita da un settore immobiliare in cui, attualmente, i prezzi risultano stagnanti o in calo. Gli analisti ritengono che per la ripresa bisognerà aspettare ancora a lungo. Pertanto, le aziende in difficoltà sono parecchie. E diversi concorrenti di Woongjin Group si sono già rivolti ai programmi di aiuto forniti dal governo.

Woongjin invece ha scelto di “sacrificare” una quota del 30% di Woongjin Coway, che è una delle sue società più redditizie. Si tratta infatti del principale fornitore di servizi domestici di depurazione dell'acqua nel Paese asiatico. Copre una quota di mercato pari a circa il 50% e i suoi margini operativi si aggirano intorno al 15%. Si prevede dunque che l'operazione attiri l'interesse di molte altre holding coreane; e, magari, anche di colossi cinesi in via di espansione oltreconfine.

[Modificato da (sylvestro) 26/03/2012 21:49] |

| |

|

| |

| 11/04/2012 15:06 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

AUSTRALIA E CANADA: BOLLE IMMOBILIARI CERCASI!

11 aprile 2012

icebergfinanza

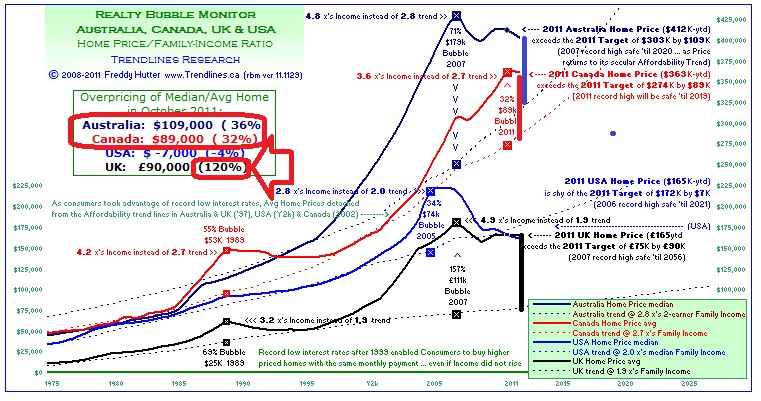

Abbiamo recentemente dato un’occhiata alla situazione di alcuni mercati immobiliari mondiali con particolare attenzione a quello che sta accadendo in Canada e Australia.

Tim Iacono su IACONORESEARCH ci racconta che secondo un’analisi relativa al mercato immobiliare di Sydney QUI quello che sta accadendo in Australia assomiglia alla California del 2005 quando si parlava di grandi opportunità invece di essere preoccupati per una crisi incombente.

“When the housing market finally popped toward the end of 2007 here in the US, the average American’s debt-to-income level was 127%,” suggest Lombardi. “In Canada, the average Canadian is setting record levels of debt-to-income among industrialized nations at 151%.”

Quando la crisi è scoppiata in America l’indebitamento medio in rapporto al reddito degli americani era del 127 % oggi in Canada invece siamo intorno al 151 % livelli record per una nazione industrializzata.

Non male vero…vi ricordate questo grafico…

“People are buying into the Canadian housing market believing that home prices ‘can’t go down,’” suggest Lombardi “This is similar to the feeling in America before US housing prices started to collapse.”

E’ incredibile come la memoria storia sia labile soprattutto quando si tratta di una memoria recentissima… i prezzi delle case non possono scendere.

In Trentino nella mia terra, questa è la sensazione prevalente ma sono anni che suggerisco di fare attenzione, non siamo diversi dagli altri, le dinamiche possono essere differenti ma nei prossimi anni mancherà la spinta propulsiva del credito e dei cosidetti compratori “principianti”.

Toronto sounds a lot like Miami, Florida in 2005 and those debt figures have forever changed how I look at our neighbors to the north.

La leggenda metropolitana della virtuose banche canadesi sembra nebbia che si dissolve al primo sole, se alcune informazioni sono giuste e attendibili, come il fenomeno “subprime made in Canada” come abbiamo visto recentemente o i recenti famigerati ” Only Interest ” della Norvegia.

Of course, it didn’t end well in California and it doesn’t look like it will have a happy ending in Canada.

Naturalmente, non è finita bene in California e sembra che non avrà un lieto fine neanche in Canada. Chi l’avrebbe mai detto ;-D |

| |

| 12/04/2012 10:04 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

|

| |

| 12/04/2012 10:28 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

|

| |

| 13/04/2012 12:21 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Investimenti globali in immobili commerciali a 75 mld $ nel I trim. 2012 (-23%)

12.04.2012

Le stime preliminari di Jones Lang LaSalle sulle transazioni dirette di immobili commerciali a livello globale mostrano un primo trimestre 2012 con volumi a quota 75 miliardi, - 23% rispetto al Q1 2011[/B].

Le previsioni annuali per il 2012 rimangono in linea con i dati del 2011, a circa 400 miliardi di dollari di transato.

|

| |

| 26/04/2012 18:56 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Apr 26, 2012

House price falls in Sweden

Swedish house prices have fallen slightly since the peak in Q1 2010. During 2011 they fell by 2.7% (4.89% in real terms) to an average price of SEK 1,969,000 (€221,316), according to Statistics Sweden.

In Greater Stockholm, average house prices fell by 4.4% during 2011 (-6.6% in real terms) to SEK 3,643,000 (€409,473), with a large fall in the last quarter when prices fell 7.9% (-8.6% in real terms).

Regions with large house price declines included Södermanland, which experienced a 8.94% decline during 2011, followed by Värmland and Östergötland with 8.6% and 7.4% price falls, respectively.

Västerbotten had the highest house price increase among Swedish regions in 2011, at 4.4%. Gotland (3.5% rise) and Uppsala (2.8% rise) also had decent house price increases.

Sweden house prices

The drop in house prices was partly influenced by the Riksbank’s seven hikes in the key rate since July 2010, to 2% (the rate prevailing between July 2011 and October 2011). These hikes were in response to strong GDP growth in 2011 (3.9% ), and high lending for house purchases, Since then, because of the slowing economy, the Riksbank’s key rate has been lowered to 1.50%.

It is likely that house prices in Sweden will slide or at best at best be stable in 2012, according to Riksbank Central Bank Governor Stefan Ingves. “The pace of lending is significantly lower now than before and we have a generally weaker economic development,” says Ingves.

Possible bubble?

Sweden’s house price boom started in mid-1990s, after the economy recovered from its financial crisis. From 1996 to 2007, the Greater Stockholm house price index soared 217% (119% in real terms). House prices rose 236% (185%) in Greater Malmo, and 202% (156%) in Greater Gothenburg over the same period. In five of Sweden’s eight regions, house prices doubled.

Sweden average house prices

The boom was set off by low interest rates, rapid economic growth and lack of new supply. With inflation stabilizing after 1995, interest rates for house purchases dropped from more than 10% during the first half of 1996, to less than 5% between 2004 and 2008. Real interest rates dropped from 7% to 2%, partly due to stiff competition between housing credit institutions, banks and other financial institutions. Housing credit lending rose from 27% of GDP in 2000, to 47% in 2011.

There was a hiccup in 2008, when the average price of houses in Sweden (one- and two- dwelling buildings) fell 0.9% (-1.7% in real terms) in the year to end-Q1 2009. In Greater Stockholm, the average price of houses fell by 5.5% (or -6.3% when adjusted for inflation).

Prices regained momentum in 2009, surging 10.3% y-o-y to Q1 2011 (9.2% in real terms).

Greater Stockholm’s average house price rose 11.4% y-o-y (10.3% in real terms).

Average house prices also increased by 12.5% (11.4% real) in Greater Goteborg, and by 14.2% (13% real) in Greater Malmo.

The OECD warned of a possible bubble in November 2011. According to the OECD, Swedish house prices were overvalued by 30% in relation to income. US economist Robert Shiller, who early on warned of the US housing bubble, also believes that Sweden may be having a housing market bubble, noting that housing prices have risen in Sweden at least as much as in the countries where prices have crashed.

Shortage in housing supply

Sweden is on a par with Europe’s supply laggards, the Netherlands and the UK, in terms of low building rates. During mid-1990s to early 2000s, there was a notable drop in dwellings built for social renting, because of free-market economic reforms.

Around 42,000 dwellings were completed annually from 1980 to 1990.

From 1995 to 2001, less than 10,000 dwelling units were completed annually

It was only in 2004 that dwelling completions again exceeded 20,000 units.

Sweden dwellings completed

Housing completions increased to 32,021 units in 2008, but this is still way below the levels of the early 1990s. With the world economic crisis, completions dropped 28% to 22,821 units in 2009. In 2010 there were only 19,500 completions; 10,625 (54%) were in multi-dwelling buildings while 8,875 (46%) were in one or two-dwelling buildings.

Housing starts picked up in 2010 with 26,000 units, but then declined to 21,000 units in 2011.

The big mortgage market expansion

Sweden lending to households

hHusing credit institutions’ lending rates fell to historic lows during the latter part of 2009 to early 2010, at around 1.6% to 2%. The lower interest rates stimulated mortgage demand and pushed up house prices. Most borrowers were on variable rate loans, which accounted for 80% of new loans in 2009.

Rates tightened in the latter part of 2010, as the economy recovered. By autumn 2011, only half new loans were variable rate, as expectations of a rate hike grew.

Mortgage lending continues to slow. Housing credit growth in 2011 was 6%, lower than outstanding loan growth of 9% in 2009, and 7.1% in 2010, respectively.

Tax reforms have encouraged home-ownership

Radical reforms in property taxation have recently significantly encouraged house-ownership:

In 2006, taxes for owner-occupied housing and tenant-ownership associations and their members were reduced - to about half of what would be required for neutrality, vis-à-vis other capital taxes and interest deductibility.

In 2007, the tax on imputed housing rent was abolished, making ownership preferable to renting (imputed rent is assessed on a rent that is deemed whether the owner actually rented the unit out or not).

In 2008, the real estate tax was replaced by a municipal fee of SEK4,500 (€481). On the other hand, the capital gains tax was raised from 20% to 30%.

Shrinking rental market?

Homeownership has been growing continuously in Sweden in recent decades, and especially rapidly in the past few years. Rented dwellings are now only 35% of all dwellings, as compared to 42% in 2010.

Owner occupied homes now account for 65% of all dwellings: 43% of those are straightforward owner occupied homes, while 22% are tenant-owned cooperative dwellings. The growth of tenant-owned co-operatives has trimmed the rental sector, as new co-operatives have taken over previously rented property, and built new dwellings. These conversions have been prevalent in major cities.

Currently, around half the rental sector is owned by municipal housing companies (MHC), non-profit companies linked to local authorities, while the other half is privately owned.

Rents in Sweden are largely historic cost-based, and reflect the age composition of the social housing stock. Swedish law requires that rent-setting be negotiated between tenant organizations and municipal housing companies (MHCs) or private landlord organizations. Private rents are compared to social housing rents, which leads to rent conformity across tenures. This has led to rental yields that are relatively low and uncompetitive.

This rent-setting structure means that in attractive central urban locations, rents are often well below market levels. This limits the profitability of the private rental market. Therefore, the private rental sector has declined significantly over the past two decades. In 2011, rents for MHCs had a 2.6% increase from the previous year, and 2.3% in the private sector.

Easing interest rates

Sweden interest rates and mortgage rates

During the second half of 2010, Swedish interest rates tightened from Europe’s lowest benchmark rate, of 0.25%. With seven rate hikes from July 2010 the benchmark interest rate was tightened to 2% in July 2011, but the Riksbank’s repo rate is down to 1.50% in March 2012, following the ECB’s latest rate cut to 1% last December 2011.

The interest rates for house purchases imposed by housing credit institutions steadily increased from 2.8% in September 2005 to 6.04% in September 2008 (due to a major change in the structure of interest rates in Sept 2005, earlier figures are not available). Housing credit institutions rates then followed the key rate downward to 1.65% in November 2009, and have now come back up to around 3.92%.

Economic slowdown in 2012

Sweden’s economy grew by 3.9% in 2011, down from 6.1% in 2010. Exports suffered from the unstable international conditions, with only a 0.6% exports increase. Low consumption also contributed to Sweden’s slowdown, with household consumption only rising 0.7% in Q4 2011, while government consumption rose 0.8%.

The government cut its 2012 economic growth forecast to 0.4% due to “problems in the public finances of several euro[zone] countries”, Sweden’s Finance Minister Andres Borg announced. However, growth is expected to pick up the following year, with 3.7% GDP growth in 2013.

Inflation remains below the Riksbank’s 2% target, at 1.9%. Meanwhile, unemployment rose to 7.8% in December 2011. Sweden’s unemployment is likely to peak at 9% next year, according to Danske Bank’s analyst Michael Grahn, paving the way for a Riksbank repo rate reduction to 0.5% this year. |

| |

| 29/04/2012 12:24 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Australian Private Debt Is At Record Level And The Housing Bubble Has POPPED, Most People Don't Know How Money Is Created (fractional reserve) And How It Can Create Asset Bubbles.. The Smart Money Is Renting And Will Buy When True Value Returns.

Money Is Debt and patience is key

For more information - Check out WRC559.com

Also Subscribe to HouseBubbleAussie

Apolgise for the poor image and audio sync. |

| |

| 29/04/2012 12:32 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

|

| |

| 03/05/2012 11:33 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Ubs: “Pericolo bolla immobiliare in Svizzera”

03/05/2012

Il pericolo di una bolla immobiliare è aumentato ulteriormente in Svizzera, secondo l'Ubs.

L’indice di riferimento, lo Swiss Real estate bubble index, calcolato dalla banca, nel primo trimestre 2012 è progredito di 0,15 punti a 0,95 punti, avvicinandosi così alla soglia di rischio.

L'Ubs considera che vi sia una situazione di rischio con valori superiori a 1.

Gli esperti dell'istituto si attendono il superamento di tale limite nel trimestre corrente.

L'indice -ricalcolato fino al 1982- aveva raggiunto il massimo di 2,5 punti all'inizio degli anni Novanta, al momento del picco dell'ultima bolla immobiliare elvetica.

Il nuovo consistente incremento è determinato dal rincaro delle abitazioni in proprietà (+6,3% per gli appartamenti e +4,6% per case unifamiliari, rispetto a un anno fa) e dall'inarrestabile crescita dell'indebitamento ipotecario, insieme alla sempre più attrattiva scelta degli immobili come opzione d'investimento.

Se si confrontano i rincari reali per un'abitazione in proprietà nella fascia di prezzo intermedia (pari a oltre il 21% di acquisto negli ultimi quattro anni) con quelli degli anni '80, l'evoluzione attuale è analoga a quella segnata nel periodo 1984-1988.

Tuttavia è possibile che i prezzi manterranno l'attuale ritmo di crescita ancora per qualche anno e che quindi il ritorno a un livello maggiormente giustificato sulla base dei dati fondamentali si traduca un periodo di flessione altrettanto prolungato.

Il numero di regioni con rischio sostanziale di correzione dei prezzi delle abitazioni in proprietà si è allargato.

In queste zone critiche vive attualmente circa il 26% dell'intera popolazione svizzera.

Considerata la loro importanza nazionale, le regioni di Zurigo (foto), Ginevra e Losanna sono ancora quelle maggiormente a rischio.

Gli importanti agglomerati di Zugo, Pfannenstiel, Zimmerberg, March, Vevey, Morges e Nyon, unitamente alle regioni turistiche di Davos e dell'Alta Engadina, rientrano pure nella categoria delle regioni critiche.

Il Ticino non è invece considerato né a rischio, né da monitorare. |

| |

| 08/05/2012 08:36 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

May 07, 2012

The Netherlands’ housing slump continues

by Lalaine Delmendo

After four years of housing market slump, in early-2012 house prices in the Netherlands continue to fall.

During the year to end-March 2012, the prices of existing homes sold in Netherlands fell by 4.7%, according to Statistics Netherlands (CBS). The average property price was €230,341 in March 2012. Over the same period:

The average purchase price of single-family dwellings fell by 6.4% to €247,206

The average purchase price of apartments dropped 4.9% to €183,213

Netherlands house price chart

This is supported by data from the Dutch Association of Real Estate Agents (NVM), showing that the average price of property sold fell by 4% y-o-y in Q1 2012, to €214,000.

House prices in the Netherlands are expected to fall by another 5% this year, amidst economic recession, according to the NVM. Almost all cities and municipalities in the country have seen their house prices falling in the first quarter of 2012. Among the major cities, Amsterdam (-3.9%) and Maastricht (-3.8%) have seen the highest house price falls, according to the CBS. Nationally, house prices fell by 2.8% in Q1.

After almost 15 years of housing boom, the Dutch housing market started to become weak in 2008, mainly due to the global financial meltdown.

In 2008, house prices fell by 5.3% (-7.5% in real terms)

In 2009, house prices dropped by 1.5% (-2.4% in real terms)

In 2010, house prices rose slightly by 1% (-0.7% in real terms)

In 2011, house prices dropped by 3.8% (-6.2% in real terms)

The Dutch economy is projected to contract by 0.5% in 2012. The economy entered recession in Q4 2011, when real GDP shrank by 0.6% both on a yearly and quarterly basis.

Housing boom and bust

The Netherlands’ house price boom lasted from 1992 to 2007, pushed by rapid economic growth. Median house prices in the Netherlands rose by about 80% (59% in real terms) from Q1 1996 to Q2 2001. Amsterdam, the capital, experienced house price growth of 111% (86% in real terms) during this period.

At the peak of the boom, national prices rose by an average of 11% (8.4% in real terms) annually from 1996-2001. During this period the economy grew 3.7% annually, and real private sector wages rose by 3.6% annually, while inflation was only 2.7%, leading to significant increases in purchasing power.

From Q3 2001 to Q1 2003, median house price growth slowed, while prices in Amsterdam and The Hague dropped. This reflected a slowdown of the Netherlands’ annual GDP growth to an average of 0.8% p.a. from 2001 to 2003. Political instability also contributed to the recession. In 2002, two governments fell (the Wim Kok government in April 2002, and the first Balkenende government in October 2002). Then the leader of the right-wing populist party (LPF), Pim Fortuyn, was killed days before the May 2002 parliamentary election.

However the Netherlands’ political and economic situation stabilized in 2003. The economy grew by an average of 2.6% annually from 2004 to 2006, and by Q2 2006, house prices in Netherlands had risen 14% (9% in real terms) on three years earlier, with strong increases in The Hague (17.5% nominal and 12.5% in real terms) and in Utrecht (15% nominal and 10% real).

Despite political crisis during the period, house prices in the Netherlands still rose by 3% from Q3 2006 to Q4 2007, propelled by economic growth of 3.45% in 2006 and 2007. Amsterdam registered the highest house price increase of 12.6%, followed by Utrecht’s 9.9% house price increase.

House prices fell by 5.3% (-7.5% in real terms) in 2008, and by 1.5% (-2.4% in real terms) in 2009, as GDP growth slowed to 1.8% in 2008, and contracted by 3.5% in 2009. Despite modest economic recovery since then (GDP growth of 1.6% in 2010, and 1.3% in 2011) the Dutch housing market has remained depressed – a situation which is expected to continue.

Building permits at lowest since 1953

netherlands-dwellings-supply

Building permits issued were down by 9% in 2011, to 55,804 - the lowest level since 1953, according to the CBS.

In 2011, the country’s total dwelling stock was up 1% from the previous year to around 7,217,803 dwellings. The total number of newly completed dwellings was up 3% in 2011 to 57,703 units, but actually down by 30.4% from 2009.

Of this total, about 6% or 417,000 units were vacant. Vacant dwellings are usually in tourist areas (e.g. West Frisian Islands), and in larger towns. Owner-occupancy is currently nearly 60% of the occupied stock, up from 42% in 1980.

Transactions have slumped

The total number of dwellings sold, at 120,739 units in 2011, is dramatically down on the average 206,000 dwellings sold annually from 2005 to 2007.

The number of dwellings sold fell to 182,392 units in 2008, to 127,532 units in 2009, and to 126,127 units in 2010.

Worse may lie ahead. In the first quarter of 2012 dwellings sold fell by 15.5% compared with Q1 last year, to about 23,951, according to CBS.

Interest rates have not fallen enough

Netherlands mortgage interest rates

The Netherlands’ house-price boom was encouraged by a reduction in mortgage interest rates from an average of 9.58% between 1990 and 1992, to 4.7% in May 1999. Rates then hovered between 5% to 7% from 2000 to 2002, dropping to 4.5% in 2003, 4.18% in 2004, and 3.16% in 2005, moving gradually up, as the ECB tightened, to mortgage rates of 5.34% in 2008.

When the global financial crisis exploded in Q3 2008. the ECB slashed the key 12-month Euribor rate from 4.81% in 2008 to 1.35% in 2010. However mortgage interest rates did not fully respond, falling only to 4.86% in 2009, and 4.52% in 2010. Now average mortgage interest rates are around 4.55%, despite a rise in the 12-month Euribor rate to an average of 1.94%

Irresponsible policies, over-mortgaged nation

Since the 1980s, the government has aggressively promoted homeownership, offering generous mortgage subsidies. The Dutch fiscal regime allows full tax deductibility of most mortgage interest payments at the marginal tax rate. The following requirements should be met for mortgage interest to be deducted from tax:

The house purchased is the main residence

The mortgage loan has a period of a maximum of 30 years

The profit made on the sale of the previous houses is used to reduce the size of the mortgage on the next one

Netherlands mortgages

Mortgage market liberalization has also brought new competition. Since 1995, 90% of new mortgages have been not repayable till loan maturity, while 30% do not have to be repaid at all (“interest-only”).

As a result, the Dutch mortgage market has expanded rapidly over the past decade. Residential mortgage debt rose to almost 100% of GDP in 2008, up from 60% of GDP in 1998. In 2011, total residential mortgages were about 106% of GDP, based on data released by De Nederlandsche Bank (DNB).

To discourage excessive mortgage growth, the government implemented the following policies:

In 2001 tax deductibility for mortgages used for non-housing consumption or investments and second-home purchases was removed.

In 2002, interest deductibility was limited to 30 years.

From January 2004, homeowners moving to more expensive homes have had to use their capital gains on their former house for down payment.

Nevertheless, mortgage growth continued in 2011, with total outstanding residential mortgages rising by 2.1%, to €639.6 billion.

According to a recent IMF report, the generous Dutch mortgage tax relief, which allows homeowners to deduct the full cost of their mortgages from tax, is distorting the housing market. It also means that Dutch banks are faced with higher risks because the large amount of tax relief encourages people to spend more on a house than they can actually afford.

Mortgage approvals falling

Netherlands mortgage shares

In 2011, the total amount of new mortgages approved rose by 15.5% to €73.3 billion from a year earlier.

However, in the last quarter of 2011, there were signs that the mortgage market is cooling. The total amount of new mortgage approvals in Q4 2011 was only €15.7 billion, down by 19.2% from the same quarter last year. This is a far cry from the €20 billion approved in Q2 2008, or the €30.9 billion approved in Q4 2005.

Most Dutch housing loans are fixed rate mortgages (FRM) for 5 years or more. However the shares of fixed and floating mortgages vary, depending on interest rates. When interest rates rapidly rose in 2007, households shifted to fixed rate mortgages. In Q2 2007, 43% of new loans had 10 year interest rate fixations (IRFs), while the share of loans with IRFs of less than 5 years dropped to 25%.

Netherlands new house loans

Social housing and the rental market

Traditionally, Holland has had a large social rental housing sector. In the 1950s, owner occupants accounted for only 29% of the housing stock.

More recently the government has been promoting home ownership, with remarkable results. Owner-occupancy rose to 42% by 1980, then to 55% by 2005. Now about 60% of the total housing stock is owner-occupied. But in many major cities (Amsterdam, The Hague, Rotterdam, and Utrecht), about 50% of the housing stock is social housing.

Homeowners receive favorable tax treatment. Aside from full income tax deductibility of mortgage interest payments; capital gains from rising house prices are also not taxed. However, this is partly offset by an annual imputed rental income tax, based on the property’s assessed value.

The government provides home-ownership grants to low-income households. Many renters also receive direct government subsidies to keep their rent-to-income ratio within certain limits.

In 2001, total government subsidies for the owner-occupied sector amounted to around €8 billion, with a similar amount provided for the rental sector. The system is highly inefficient in terms of social objectives. It also reduces mobility both for owner-occupiers and renters.

Of the total increase in dwelling stock of 65,339 units in 2011, about 40.6% are rented houses. A huge proportion of rented accommodation is owned and managed by housing corporations. They manage about 2.4 million dwellings.

Free market yields are good

Netherlands house prices and inflation

Rent increases in rent-controlled dwellings are set to a maximum, equivalent to last year’s inflation. About 95% of the rental stock falls under this special regulatory framework (see Landlord and Tenant section). A landlord may impose rent increase once a year, but the government sets the maximum rental rate increases.

With inflation-based allowable rent increases generally lagging behind price increases, rental yields are generally low to moderate in the Netherlands. The maximum allowable rent increase from July 1, 2011 to June 30, 2012 was 1.3%, in effect capping rents at €630 per month.

In theory, only individuals with an annual income of below €34,000 are entitled to rent-controlled dwellings. However, a large number of high earners benefit from these rent-controlled properties. Because of this, a new law is being proposed which allows landlords to increase the rent of high earners by an extra 5% above the inflation level. However, it is still unclear when this new law will take effect.

In the small up-market decontrolled sector, which consists of around 5% of all rental dwellings. gross rental yields can be good. Non-controlled rents rose by 4.2% in 2011. Rental yields on non-controlled apartments in Amsterdam varied from around 4.4% on 250 sq. m. apartments in 2011, to around 6% on 70 sq. m. apartments, according to the Global Property Guide.

In The Hague, rental yields were somewhat higher, at around 6% on 200 sq. m. apartments, to nearly 7% on 85 sq. m. apartments.

Depressed economy

Netherlands gdp growth and unemployment

The Dutch economy is expected to contract by 0.5% in 2012, having entered recession in Q4 2011, when real GDP shrank by 0.6% both on a yearly and quarterly basis.

Unemployment is rising. In 2012, the percentage of unemployed is expected to rise to 5.5%, up from an average of 3.46% from 2007 to 2009, according to the IMF. Despite this, the Netherlands has one of the Eurozone’s lowest unemployment rates.

During the recession, the government was forced to boost the economy through stimulus programs and bank bailouts, which resulted in a budget deficit of 4.6% of GDP in 2009, 5.1% of GDP in 2010 and 4.8% in 2011. As a result, the country’s debt rose to 65.2% of GDP in 2011.

The government now plans to enact about €15 billion (US$20 billion) in new austerity measures to bring the country’s budget deficit in line with EU rules. The government is expected to implement tax increases and spending cuts on welfare and health care. In addition, it is also expected to address the country’s huge mortgage debt. |

| |

| 15/05/2012 07:36 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

click per ingrandire

|

| |

| 25/05/2012 23:15 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Global house price downturn accelerates: Q1 2012

by GLOBAL PROPERTY GUIDE

May 25, 2012

The world's housing markets moved clearly down during the year to the first quarter of 2012, according to the Global Property Guide's latest house price indices survey. House prices fell in 24 countries, of the 36 countries for which quarterly house price statistics are available, and rose in only 12 countries.

Source: Various series, data descriptions and sources here

During the latest quarter the downturn appears to have accelerated, with house price falls in 26 countries, and house price gains in only 10.

In nominal terms only 16 countries experienced house price falls during the year, while 20 countries recorded house price rises. But the Global Property Guide's statistical presentation uses price changes after inflation, giving a more realistic picture than the more upbeat nominal figures usually preferred by real estate agents.

Faster-paced deterioration in European housing markets

Ireland's price-declines have been, over the duration of the crisis, catastrophic. It is disheartening to see more agony, yet the picture really is alarming. House prices fell 18.95% year-on-year, contrasting with a decline of 'only' 13.12% during the same period last year. Furthermore, house prices were down 5.19% during the latest quarter. Tough credit conditions, an oversupply of housing, and weak domestic demand have weighed down the Irish residential property market.

Source: Various series, data descriptions and sources here

There was also an alarming increase in momentum of house-price declines in Athens, Greece (-11.68%); in Warsaw, Poland (-10.94%); in Portugal (-10.45%); in Spain (-9%); in the Netherlands (-6.05%); and in the Slovak Republic (-5.89%).� All saw bigger house-price declines this year than the previous year.

Several countries whose housing markets were last year either in recovery or only just in downturn, saw a significant deterioration in their position, with house price falls during the year to end Q1 2012 in Finland (-2.05%), in Turkey (-2.32%), Sweden (-5.34%) and Riga, Latvia (-5.83%).

In other European countries, any positive changes in the momentum of the housing markets were so feeble, that they hardly signal a recovery. These countries include Kiev, Ukraine (-2.51%), Croatia (-2.45%), United Kingdom (-3.14%), Lithuania (-3.87%) and Bulgaria (-6.21%).

Some strong European markets do relieve the gloom. In Estonia house prices surged by 9.13% year-on-year, and in Austria house prices rose by 8.24% year-on-year. In fact the upsurge in these two countries' housing markets was so strong as to propel them into third and fourth place in the worldwide league table.

Other strong housing markets over the past twelve months include Switzerland (+5.49%), Norway (+5.43%), Russia (+3.86%) and Iceland (+2.25%). The 'gainers' seem to be countries whose housing markets either never experienced the recent downturn (Austria, Switzerland, Norway), or are recovering (Estonia, Russia, Iceland).

House prices in India (Delhi) and Brazil (Sao Paulo) surged further, but momentum down during the quarter

Over the year to Q1 2012, Delhi house prices skyrocketed by 24.41%, though during the last quarter, they fell 0.07%. Some other Indian cities like Chennai and Kolkata saw house price falls year-on-year, according to NHB Residex.

In Sao Paulo, house prices climbed by 18.70% in the year to Q1 2012, but the latest quarter saw a price-decline of 2.57%.

Most Asian housing markets slowing

In the Philippines (Makati Central Business District), prime condominium prices rose by 7.34% during the year. But the figures possibly exaggerate the upsurge, because they are for Makati, the heart of the Philippines' business process outsourcing boom. In South Korea house prices were up 2.67% from a year earlier.

Housing markets in the rest of Asia cooled over the year to Q1 2012, due to government measures implemented last year. House prices in Hong Kong were up a mere 0.19% on the year, after a rise of 19.80% the previous year.� There were house price falls in Indonesia (-0.13%), Singapore (-1.36%), Tokyo, Japan (-2.64%) and Shanghai, China (-3.68%).

US housing market making progress

US house prices rose modestly to 0.48% year-on-year, with a quarterly rise of 0.55%, according to the Federal Housing Finance Agency's (FHFA) seasonally adjusted purchase-only house price index. In inflation-adjusted terms, US house prices were still down 2.27% from a year earlier. But this is a significant improvement from last year's 7.44% decline in house prices.

Increased affordability and a somewhat smaller inventory of homes for sale are positively impacting house prices, says FHFA Principal Economist Andrew Leventis.

Israeli house prices weakening

House prices in Israel were down 4.94% year-on-year to Q1 2012. Prices were hit by worldwide uncertainty, plus measures taken by the Israeli government and the Bank of Israel. The fall comes amid popular protests since last summer over high prices, which have not yet waned.

New Zealand firm, but Australia under pressure

House prices in New Zealand climbed by 0.82% over the year to Q1 2012, after falling 4.79% the previous year. Sales activity has been strong for the last few months, with volumes at the highest levels since 2007.

Australian house prices fell for the fifth straight quarter to -6.04% from a year earlier, the longest downturn for a decade. The central bank has maintained the highest borrowing costs among major developed nations.

|

| |

| 27/05/2012 18:00 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

|

| |

| 30/05/2012 16:53 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Islanda, a quattro anni dal default si teme la bolla immobiliare

30 Maggio 2012

L'Islanda ha stupito il mondo per il clamoroso default con cui nel 2008 si è dichiarata insolvente ed è sprofondata nella recessione. Ma l'ha stupito anche per la rapidità della sua ripresa. Ora, però, torna l'allarme: stando all'agenzia Bloomberg, non sono pochi gli analisti che evidenziano il rischio di una nuova, pericolosa bolla immobiliare.

Nel 2008, per evitare un esodo di massa, il governo ha imposto alcune restrizioni sulle operazioni in valuta estera. Dunque, secondo gli esperti, si aggirano ormai intorno agli 8 miliardi di corone (61 milioni di dollari) i capitali “bloccati” nell'isola. Stando ai segnali del governo, tali restrizioni continueranno almeno fino al 2015. Gli investitori, così, puntano su una delle poche opzioni rimaste: il real estate. Ciò – ritengono in molti – potrà avere una sola conseguenza: un'imminente bolla immobiliare. I dati sembrano andare in questa direzione. Stando alle fonti ufficiali, nell'ultimo trimestre i prezzi per le case nuove sono saliti addirittura del 40,1% rispetto all'ultimo trimestre del 2010.

Quella attuale, per l'economia dell'isola nordica, è una fase di espansione. Si prevede che il pil cresca del 3% quest'anno e del 3,9% nel 2013. Per il Vecchio Continente, al contrario, la Commissione europea stima nel 2012 una contrazione dello 0,3% e nel 2013 una crescita solo dell'1%. Ma il sistema rischia il surriscaldamento. A guidare la ripresa sono stati anche i consumi delle famiglie, che hanno fatto impennare il volume di debito privato. Da agosto, quindi, la banca centrale ha alzato a più riprese il tasso d'interesse, che ora è pari al 5,5%. Se si tiene inoltre presente che la maggior parte dei mutui è legata all'indice dei prezzi al consumo che ad aprile è cresciuto del 6,4% su base annua, ciò significa che i prestiti, per le famiglie, risultano sempre più onerosi. E ci si chiede se le autorità debbano fare qualcosa per fermare l'insorgere della bolla.

|

| |

| 01/06/2012 10:30 |

|

| | | Post: 90 | Città: TORINO | Età: 48 | Sesso: Maschile | Utente semplice | Sottoscala | | OFFLINE | |

|

Sgonfiamento bolla in Romania Non ho piu scritto da qualche tempo, ma continuo a seguirvi :)

Oggi e uscito un in giornale principale della Romania un nuovo articolo sul callo dei prezzi immobiliari in Romania (ne escono 2-3 al mese). L'articolo potete trovarlo qui. La parte interessante e invece l'immagine sotto:

I prezzi indicati sono in euro per Bucarest, rilevati nel mese di maggio di ogni anno indicato. Si parte dai monolocali/bilocali in alto, trilocali quattro locali e cinque locali (in Romania si contano le stanze, la cucina non viene contegiata). Si osserva che i prezzi sono circa a 50% del massimo del maggio 2008.

Aspetto tale discesa anche qui ![[SM=g1784310]](https://im1.freeforumzone.it/up/17/10/756547440.gif)

[Modificato da rumburak 01/06/2012 10:31] |

| |

| 01/06/2012 12:12 |

|

|

Re: Sgonfiamento bolla in Romania rumburak, 6/1/2012 10:30 AM:

Non ho piu scritto da qualche tempo, ma continuo a seguirvi :)

Oggi e uscito un in giornale principale della Romania un nuovo articolo sul callo dei prezzi immobiliari in Romania (ne escono 2-3 al mese). L'articolo potete trovarlo qui. La parte interessante e invece l'immagine sotto:

I prezzi indicati sono in euro per Bucarest, rilevati nel mese di maggio di ogni anno indicato. Si parte dai monolocali/bilocali in alto, trilocali quattro locali e cinque locali (in Romania si contano le stanze, la cucina non viene contegiata). Si osserva che i prezzi sono circa a 50% del massimo del maggio 2008.

Aspetto tale discesa anche qui

I cali arrivano anche al 60% ![[SM=g7840]](https://im0.freeforumzone.it/up/0/40/4492320.gif) |

| |

| 01/06/2012 12:55 |

|

| | | Post: 3.963 | Città: ROMA | Età: 56 | Sesso: Maschile | Utente semplice | Castelletto sul Ticino | | OFFLINE |

|

Re: Re: Sgonfiamento bolla in Romania dgambera, 01/06/2012 12.12:

I cali arrivano anche al 60%

deja vu - mi stupisce piuttosto la tenuta dei tagli grandi, "migliore" di quelli piccoli

notare anche il supergradino del 2009, altro che cali del 4% annuo... [Modificato da _gmp_ 01/06/2012 12:56] ***************************

Never a better time to buy! |

| |

| 01/06/2012 13:30 |

|

| | | Post: 90 | Città: TORINO | Età: 48 | Sesso: Maschile | Utente semplice | Sottoscala | | OFFLINE | |

|

Re: Re: Re: Sgonfiamento bolla in Romania _gmp_, 6/1/2012 12:55 PM:

deja vu - mi stupisce piuttosto la tenuta dei tagli grandi, "migliore" di quelli piccoli

notare anche il supergradino del 2009, altro che cali del 4% annuo...

E stiamo parlando di Bucarest, dove il mercato immobiliare e fra i piu movimentati in Romania ... Nelle altre citta c'e anche di peggio (a partire da interi palazzi abandonati in citta miniere che sono diventati citta fantasma in seguito alla chiusura delle mine, fino a grandi progetti residenziali lasciati non finiti in giro nelle grandi citta in seguito a falimento del costruttore). |

| |

| 01/06/2012 15:17 |

|

|

Re: Re: Re: Re: Sgonfiamento bolla in Romania rumburak, 6/1/2012 1:30 PM:

E stiamo parlando di Bucarest, dove il mercato immobiliare e fra i piu movimentati in Romania ... Nelle altre citta c'e anche di peggio (a partire da interi palazzi abandonati in citta miniere che sono diventati citta fantasma in seguito alla chiusura delle mine, fino a grandi progetti residenziali lasciati non finiti in giro nelle grandi citta in seguito a falimento del costruttore).

e delle quotazioni dei terreni che mi dici?

|

| |

| 01/06/2012 15:18 |

|

| | | Post: 3.963 | Città: ROMA | Età: 56 | Sesso: Maschile | Utente semplice | Castelletto sul Ticino | | OFFLINE |

|

Re: Re: Re: Re: Re: Sgonfiamento bolla in Romania dgambera, 01/06/2012 15.17:

e delle quotazioni dei terreni che mi dici?

![[SM=g9128]](https://im0.freeforumzone.it/up/0/28/3140032.gif)

***************************

Never a better time to buy! |

| |

| 03/06/2012 18:38 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

3 giugno 2012

Compravendite in calo: mercato immobiliare in profondo rosso

In calo i prezzi,ma in calo anche le vendite: il mercato immobiliare sloveno, in questo momento, non gode di buona salute.E non ci sono segnali, considerato che siamo in piena crisi economica, che le cose possano migliorare in tempi brevi. I dati pubblicati in questi giorni dall’Ufficio geodetico e dall’ Ufficio di statistica della Slovenia evidenziano questa situazione di disagio con molta chiarezza: i prezzi delle abitazioni sonoscesi inmedia del 4,2% rispetto all’ultimo trimestre del 2011.

In particolare, sono calati dell’8% i prezzi delle abitazioni nuove. Un calo più accentuato – del 10,4% – era stato registrato solo nel primo trimestre del 2009. Oggi, pertanto, in Slovenia le abitazioni nuove costano il 19% in meno rispetto al periodo record (luglio–settembre del 2008) e l’8,4% in meno rispetto a un anno fa. A livello dell’intero paese, questo significa che un metro quadro di superficie abitativa – parliamo di appartamenti in condomini, non di case – viene venduto in media per 1.689 euro.

Solo nella capitale Lubiana e sulla costa, dunque nei comuni di Capodistria, Isola e Pirano, il prezzo supera i 2.400 euro per metro quadro, e precisamente 2.404 a Lubiana e 2.468 sulla costa. Nel 2010, per fare un esempio, a Capodistria il prezzo di un metro quadro di appartamento aveva raggiunto i 2.738 euro. In altre parole, un’abitazione di 50 metri quadri, per restare all’esempio di Capodistria, oggi si può acquistare per oltre 16mila euro in meno rispetto a un anno e mezzo fa.

Il calo dei prezzi non ha portato però a un aumento della richiesta, per cui sono in flessione anche le vendite. Nei primi tre mesi del 2012, in tutta la Slovenia sonostati venduti 1.464 appartamenti in condomini e 679 case, contro i 1.821 appartamenti e le 981 case vendute nell’ ultimo trimestre del 2011. Una scossa al mercato immobiliare potrebbe arrivare nelle prossime settimane. Il Fondo alloggi sloveno ha annunciato infatti l’intenzione di investire 40 milioni di euro per l’acquisto di appartamenti attualmente vuoti per poi rivenderli o affittarli a equo canone. Gli esperti però sono scettici: si tratta di denaro, sostengono, che non finirà nel settore edile, attualmente in crisi, ma nelle banche, che sono proprietarie di centinaia di alloggi che le aziende edili gli hanno ceduto perché non erano in grado di pagare i propri debiti. Dal Fondo però è giunta immediata la replica: non hanno nessuna intenzione di usare i loro mezzi per acquistare case a prezzi gonfiati. |

| |

| 04/06/2012 10:12 |

|

| | | Post: 90 | Città: TORINO | Età: 48 | Sesso: Maschile | Utente semplice | Sottoscala | | OFFLINE | |

|

Re: Re: Re: Re: Re: Sgonfiamento bolla in Romania dgambera, 01/06/2012 15.17:

e delle quotazioni dei terreni che mi dici?

Non conosco il mercato dei terreni a Bucarest, ma in genere il prezzo dei terreni e sceso anche del 70-80%. Dipende molto dalla posizione (leggersi quelli in grandi citta, dove la salita dei prezzi e stata molto rilevante, sono scesi molto di piu di quelli magari nelle piccole citta dove i prezzi sono saliti di meno). Ci sono tanti che hanno investito in terreni per cercare disperatamente adesso di vendere e non trovare compratori. Grossi progetti immobiliari non partono piu (ci sono quelli faliti che convengono di piu - si parte gia con tutta la parte buracratica risolta e magari anche parte della costruzione gia fatta) e quindi i terreni sono molto difficili da vendere. Quelli piccoli (o frazionabili) si riesce ancora a vendere a famiglie che vogliono aprofitare del prezzo basso per le costruzioni per farsi la casa in proprio, ma terreni piu grossi sono pratticamente impossibili da vendere. |

| |

| 04/06/2012 10:27 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Re: Re: Re: Re: Re: Re: Sgonfiamento bolla in Romania rumburak, 04/06/2012 10.12:

Non conosco il mercato dei terreni a Bucarest, ma in genere il prezzo dei terreni e sceso anche del 70-80%. Dipende molto dalla posizione (leggersi quelli in grandi citta, dove la salita dei prezzi e stata molto rilevante, sono scesi molto di piu di quelli magari nelle piccole citta dove i prezzi sono saliti di meno). Ci sono tanti che hanno investito in terreni per cercare disperatamente adesso di vendere e non trovare compratori. Grossi progetti immobiliari non partono piu (ci sono quelli faliti che convengono di piu - si parte gia con tutta la parte buracratica risolta e magari anche parte della costruzione gia fatta) e quindi i terreni sono molto difficili da vendere. Quelli piccoli (o frazionabili) si riesce ancora a vendere a famiglie che vogliono aprofitare del prezzo basso per le costruzioni per farsi la casa in proprio, ma terreni piu grossi sono pratticamente impossibili da vendere.

Grazie ancora per la testimonianza ![[SM=g1750826]](https://im1.freeforumzone.it/up/17/26/500736236.gif)

|

| |

| 08/06/2012 12:15 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

May 30, 2012

Bulgarian house price falls continue, but at a slower pace

Bulgaria house prices

After three years of house price falls, the Bulgarian housing market remains in the doldrums.

During the year to end-Q1 2012, the average price of existing flats in Bulgaria dropped by 4.3% to BGN884 (€452) per square metre (sq. m.), after price falls of 6.4%, 6.1% and 6.2% over the year to the previous three quarters, according to the National Statistical Institute (NSI). Property prices in Bulgaria are 38% lower than the Q3 2008 peak of BGN1,418 (€725) per sq. m..

In Sofia, the capital, the average price rose by 0.8% q-o-q in Q1 2012 to BGN1,465 (€749) per sq. m., but there was still a y-o-y fall of 2.1%. Compared to the housing price peak of Q3 2008, the average price in Sofia has now fallen by 38% (-41% inflation-adjusted).

A massive house price boom led prices to surge by around 300% from 2000 to 2008. However, contagion from the global financial crisis caused the Bulgarian property bubble to burst by end-2008.

In 2009, the average price of existing dwellings plunged by 26.3% (-26.4% inflation-adjusted) from a year earlier

In 2010, house prices dropped by 5.6% (-9.5% inflation-adjusted) from the previous year

In 2011, the average price of existing dwellings fell by 6.2% (-9% inflation-adjusted) from a year earlier

In 2011, there were a total of 13,953 dwellings completed in Bulgaria, down by 11.5% from a year earlier and down by 36.7% from 2009.

The economy grew by a modest 1.7% in 2011, from a GDP growth of 0.4% in 2010 and a contraction of 5.5% in 2009.

In 2012, the Bulgarian economy is expected to slow to 0.5%, due to the eurozone debt crisis, and so Bulgaria’s housing market is expected to remain depressed in 2012.

Sofia province has rebounded strongly

Bulgaria House Price Change 2009 2010

The situation looks better in Sofia, the capital city. For the first time since Q3 2008, the average price of existing dwellings rose by 2.2% q-o-q to Q3 2010. However, the average price of BGN1,593 (€815) per sq. m. was lower by 2.9% from a year earlier.

Of the other 27 provinces, six registered positive annual price changes in Q3 2010; including Sofia Province with an impressive rebound of 22.2% increase. On a quarterly basis, house prices in 11 provinces posted increases.

Foreign demand has fallen off a cliff

Bulgaria FDI flow graph

A large part of foreign investments (FDI) entering Bulgaria in recent years went into real estate, and these have shrunk dramatically. Real estate FDI was only €61 million in Q1 2010, down from €182.2 million a year ago, and massively down from the peak of €853.6 million of Q3 2007.

The housing downturn in Bulgaria started when the global financial crisis hit Europe in late 2008.

Sales are picking up

Despite the weak prices, some agents say sales surged by 40% in Q1 compared to the same quarter last year. According to Colliers Bulgaria, sales began to pick up as early as August 2009, after months of stagnation. Houses priced below €1,000 per square metre were the most marketable.

British and Russians are the top foreign buyers of Bulgarian real estate, buying holiday houses near the Black Sea and the Danube River. Hit by the financial crisis, in Q1 2010 there was a net outflow of €30 million of UK investment from Bulgaria, in sharp contrast to the inflow of €129.8 million in Q1 2009.

Russians remain net buyers. There was an investment inflow from Russia of €43.6 million in Q1 2010, down from €73.7 million the year earlier, in Q1 2009.

The economy has emerged from recession

Bulgaria gdp growth graph

Bulgaria’s GDP rose 0.3% seasonally-adjusted q-o-q to Q3 2010, after a 0.5% expansion in Q2. From a year earlier, the economy expanded 0.2% in Q3 after a -0.3% in Q2 and -0.8% in Q1 2010. The over-all change in GDP for 2010 is expected to be around -0.5%.

Economic growth is expected to accelerate in 2011, with a GDP expansion of 2.6%. Then 3.2% growth is likely in 2012, according to the European Commission.

Unemployment is expected to climb to 9.8% by the end of 2010, from 6.3% in 2008 and 9.1% in 2009. Unemployment is anticipated to ease slightly to 9.1% in 2011 and 8% in 2012.

The global financial crisis sent Bulgaria into recession in 2009. After growing by 6% in 2008, the Bulgarian economy shrank 5% in 2009. Exports, consumption and capital formation were all down. The economy continued to deteriorate in Q1 2010, with GDP down by 4% from Q1 2009 – the second largest GDP fall among European Union countries.

Bulgaria dwellings completed graph

The unemployment rate rose to 10.2% in Q1 2010, significantly higher than last year’s 6.8%. This was also the highest since 2006.

Many housing construction projects have been halted. Dwellings completed in Q1 2010 were 26.9% down from Q1 2009, and building permits were 32.8% lower. But the really significant decline had happened a year earlier - Yambol and the capital city of Sofia had huge declines of more than 70% year-on-year to Q1 2009.

The struggling mortgage market

Bulgaria outstanding housing loans graph

Weak credit demand and stringent loan policies have meant a decrease in the amount of housing loans New housing loans granted from January to May 2010 amounted to BGN501.3 million, 4.9% higher than during the same period last year, but 65.9% lower than during the same months in 2008.

In May 2010, non-performing housing loans reached BGN 48.6 million, or 13.1% of the Bulgaria’s total bad debts. In response, banks lowered the maximum loan-to-value ratio to 50%, and have implemented strict income and property requirements.

Bulgaria interest rates graph

The average mortgage interest rate in May was down to 8.55%, from 10.09% in 2009, for BGN-denominated loans. Euro-denominated loan rates were down to 8.29%, from 8.59% in 2009. |

| |

| 13/06/2012 15:00 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Mercato immobiliare calano i prezzi ma pochi gli affari

12 giugno 2012

POLA. Sul mercato immobiliare istriano si avverte qualche incoraggiante segnale di ripresa ma non uniforme sul territorio bensì a macchia di leopardo per cosi dire. Probabilmente gli acquirenti vengono incoraggiati dal calo dei prezzi che negli utimi 4 anni ha toccato addirittura quota meno 40%. Navigando su internet e contattando direttamente le agenzie del settore vediamo che è il territorio parentino quello più vitale dove gli immobili maggiormente richiesti sono quelli destinati all'affitto turistico: appartamenti e abitazioni sul mare di superficie medio-piccola, case in pietra istriana da ristrutturare e ville urbane.

Qualche prezzo: nel centro di Parenzo si va da 2.000 a 3.000 euro al metro quadrato per scendere a 1.500 – 1700 euro a qualche chilometro fuori città. Le vecchie case in pietra da 70 a 100 mq con cortile, nei villaggi dell'entroterra che poi vengono trasformate in agriturismi o luoghi di riposo nel segno della tranquillità, si possono trovare per 50 mila euro. Poi ovviamente bisogna investire per la ristrutturazione. Gli acquirenti sono per lo più italiani, austriaci, tedeschi e sloveni che vogliono cosi crearsi una dimora fissa per le vacanze oppure da affittare.

Tra Umago e Cittanova gli immobili più richiesti sono gli appartamenti e alloggi collocati sulla prima e seconda fascia sul mare e anche in questo caso la destinazione è turistica.

Il prezzo massimo è di 2.100 euro al metro quadrato che gradualmente scende più ci si allontana dal mare. Anche in questo caso gli acquirenti sono in massima parte stranieri.

Il mercato maggiormente in crisi lo troviamo nell'area urbana di Pola dove praticamente non c'è richiesta da parte degli acquirenti, scoraggiati soprattutto dalla mancanza di parcheggi e dai prezzi che comunque rimangono alti. Tuttavia si possono trovare appartementi già a partire da 900 Euro/mq. In questa parte d'Istria gli acquirenti sembrano privilegiare i rioni cittadini periferici dove si può parcheggiare sotto casa oppure le località sul mare del circondario come Medolino, Promontore e Fasana dove i prezzi vanno da 1.600–2000 euro al metro quadrato.

In tutto questo quadro va tuttavia precisato che non ci si attende molto da qui in avanti da parte degli italiani vista la recente normativa del governo Monti che tassa anche la proprietà di case all’estero. (p.r.) |

| |

| 19/06/2012 06:51 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Apr 24, 2012

Cyprus housing market slump continues

Cyprus house pricesCyprus property prices continue to decline, the house price boom having halted in late 2008. At end-2011, Cyprus house prices were 14.5% down on their Q3 2008 peak (-20.5% in real terms), according to the Central Bank of Cyprus (CBC). This year the housing market is expected to suffer yet more, due to the recession.

Cyprus’ residential property price index fell 5.61% during 2011 (-8.87% in real terms). Apartments suffered a 7.2% price drop, while house prices fell 4.7%.

Famagusta had the largest price drop among Cyprus districts, falling 10.7% during 2011, followed by Larnaca (-8.8%) and Paphos (-8%). Nicosia had the lowest price fall of 2% during the same period, according to CBC.

Nicosia’s average house price fell 3.19% from €511,642 in Q4 2010, to €495,341 in Q4 2011, according to the Royal Institution of Chartered Surveyors’ (RICS-Cyprus) price index.

Sales continue to decline, despite government efforts to provide more consumer protection for homebuyers. Domestic sales declined 13% April to April 2012. Sales were down in all districts except Paphos, according to the Department of Lands and Surveys.

Cyprus tourism revenue graph

Although revenue for tourism increased in 2011, overseas property sales still fell 21% y-o-y, from 151 contracts to 119 in April 2012, because of the ailing UK economy (70% of all foreign buyers are British) and Cyprus’ tarnished reputation for questionable Title Deeds.

The European Commission has forecast a 0.5% contraction in Cyprus’ GDP in 2012. University of Cyprus Economic Research Centre experts see a contraction of 1.5% to 2% in 2012.

Housing market scandals

Property scandals have hit epidemic proportions in Cyprus, involving fraudulent transfers of property, the deliberate withholding of Title Deeds, and an across-the-board amnesty for development projects of dubious legality.

Title Deeds (or "Certificates of Registration of Immovable Property") are legal documents all property owners in Cyprus are required to possess. Many buyers dispensed with them in order to avoid the payment of Property Transfer Fees which, as of May 2012, is calculated as follows:

3% on the first €85,430

5% on the next €85,430

8% on the remainder

Source: Cyprus Property Law

The difficulties involved with not having a Title Deed, however, are myriad. Technically one does not own the property, despite having paid for it in full. The legal owner (the one who actually holds the Title Deed) retains the right to mortgage the property without the consent of the buyer. If the land was already mortgaged before it was sold, the legal owner can extend or increase the mortgage without consent.

Around 40,170 foreign buyers’ properties were caught in this Title Deed trap by the end of November 2011, according to the Department of Lands and Surveys. Out of 51,654 properties purchased by non-Cypriots from year 2000 to November 2011, title deeds have been transferred on only 11,484, and the gap between the number of properties sold to foreigners and Title Deed figures continues to widen.

The most insidious problem is unscrupulous property developers extorting money and claiming it as payment for "immovable property tax". This has attracted the attention of the European Union, spurred by a rising number of complaints from overseas buyers frustrated with a lack of consumer protection from developers who sell property without the proper permits and permissions—or, in one well-documented case, sell the same property twice.

The Town Planning Amnesty law

The government passed a “Town Planning Amnesty” law in April 2011, allowing illegally built properties and properties suffering from planning infringements to apply for Title Deeds. This was actually four bills to increase consumer protection.

The new planning amnesty laws:

Require the developer to move towards securing Title Deeds for his customers and carry out necessary things to ensure the Deeds issuance in a timely manner.

If a property has been completed to specification and has no planning irregularities, the project architect may file plans for a division.

Major planning irregularities should be corrected, if there are any.

The buyer or developer can submit a form of intent to go through the “planning amnesty” process if there are minor planning irregularities by October 8, 2011.

Providing that any planning infringements fall within the scope of the amnesty provisions, the applicant will be able to apply for a ‘Certificate of Final Approval’ – necessary in the process of Title Deeds issuance

Depending on the nature and extent of any infringements, a fine may be payable.

If there is a major planning infringement, it will result to an issuance of a Title Deed containing a statement about the offending part of the property. Depending on its severity, the statement may allow its sale as long as certain conditions are met, or worse, prevent the sale of the property.

Included in the planning amnesty is an immovable property sales law, which effectively gives the property owner a land contract, and removes his liability for the developer’s bad debts.

The government has also reduced VAT for first-time buyers, cutting VAT on homes up to 275 sq. m. to 5%, from the previous 15%.

Natural gas discovery

In December 2011 a gas field was discovered off the coast of Cyprus by Noble Energy Inc., involving 5-8 trillion cubic feet of natural gas in a field covering 40 square miles. The gas find was dubbed as “historic” by Cyprus President Demetris Christofias, and is worth tens of billions. It could provide the Island with electricity for 210 years according to Commerce Minister Praxoulla Antoniadou. Shortly after the discovery, Noble Energy announced plans to build a gas terminal in Cyprus.

Turkey has however already announced that it wants its share of the gas deposits. In September 2011, Turkish Prime Minister Tayyip Erdogan demanded that Cyprus postpone offshore drilling, and warned that he would send warships. Yet despite the possibility of conflict, the Government of Cyprus remains committed to the project. “Cyprus is in a position to strengthen the energy security of the EU as we are the only country in the region [with gas] that belongs to the EU,” said Antoniadou.

Low rental yields

Rental yields in Cyprus are low, compared to yields overseas, according to RICS-Cyprus. Average gross rental yields in Q4 2011 were around 3.8% for apartments, and 2% for houses. This parallels Global Property Guide research of January 2011, which found yields ranging from 2.7% to 4.6%. Larnaca has the highest yields, ranging from 4.54% to 4.76%.

Costs of buying a 120 square metre (sq. m.) apartment in Cyprus:

Nicosia: average price: €1,646/ sq. m. Rental yield: 4.35%.

Limassol: average price €2,140/ sq. m. Rental yield: 4.10%.

Paphos: average price €1,780/ sq. m. Rental yield 2.71%.

Larnaca: average price €1,330/sq. m. Rental yield 4.54%.

Tight credit market

Cyprus interest rates

Tighter credit standards were implemented by Cypriot banks during the first quarter of 2012 as a precautionary measure. In February 2012, the average lending rate for loans up to 1 year increased to 6.76%. The interest rate for loans from over 1 and up to 5 years was raised to 7%, and to 5.14% for loans over 5 years.

Variable-rate mortgages account for 97.8% of all housing loans in Cyprus, making the market vulnerable to interest rate shocks.

Cyprus’ interest rates are now among Euro area’s highest, and are relatively high In comparison to ECB rates (see chart below). Banks in Cyprus have been slow to respond to ECB interest rate cuts, and there is a big margin between the Central Bank key rate and their interest rates. That is because there is little inter-bank lending, so banks rely on customer deposits for funding. Many banks pay high rates to attract deposits, according to finance minister Makis Keravnos.

Cyprus housing loans

The adoption of the Euro in January 2008 led to a significant change in the method of calculating interest rates (from May 2008), and the data are now harmonized to the European Central Bank’s requirements.

Mortgage loans have grown significantly from 7% of GDP in 2005, to 62% of GDP in 2009. However, growth slowed down in 2010 and 2011, with 64% and 63% of GDP, respectively.

Economic contraction in 2012

Cyprus GDP graph

Cyprus’ GDP declined by 1.9% in 2009, but the country rebounded from recession with growth of 1.1% in 2010, and 0.5% in 2011. But since then Cyprus has suffered from Greece’s economic troubles, from its mortgage and corporate lending slowdown, and from increased electricity costs due to a power plant explosion. Cyprus’ unemployment has already risen to 10% in March 2012, from 6.9% in March 2011. Meanwhile, Cyprus’ annual inflation slightly declined, to 3.1% in April 2012.

Cyprus’ economic decline is likely to continue in 2012.

Recent bad news has included:

A country credit rating cut in May 2011, from AA- to A-, by Fitch

Cyprus’ top three banks were downgraded by Moody’s in November 2011

Cyprus government’s bond ratings were cut by Moody’s to junk status in March 2012, from Baa3 to Ba1, and put on negative outlook.

In coming up with this decision, Moody’s considered ”the increased risk that the Cypriot government would have to provide renewed financial support to the country’s banks because of their exposure to the Greek government and economy, and the commensurate impact of such measures on the government’s own financial strength.” |

| |

| 19/06/2012 07:03 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

Cina, calano i prezzi immobiliari

18 Giugno 2012

In Cina i prezzi delle case, nel mese di maggio, sono scesi in 54 delle 70 città monitorate dal governo. Il calo più consistente si è registrato a Wenzhou, con -14% rispetto all’anno precedente, mentre Pechino e Shanghai hanno riportato un declino che si aggira intorno all’1,6%. A riferirlo è l’agenzia Bloomberg, che cita i dati diffusi nella giornata di oggi dall’Ufficio nazionale di Statistica.

L’esecutivo di Pechino ha promesso – nonostante il generale rallentamento dell’economia del gigante asiatico – di mantenere attive le restrizioni applicate al mercato immobiliare in risposta al boom, che ha fatto temere gli effetti dell’eventuale scoppio di una bolla speculativa. Si tratta ad esempio di limiti al numero di abitazioni che ciascun acquirente può comprare, o dell’imposizione di anticipi più alti.

Bloomberg riporta l’opinione di Peter Churchouse, di Portwood Capital: «Il mercato immobiliare cinese si sta lentamente avvicinando al fondo della sua discesa e mi aspetto di assistere a un atterraggio nell’arco dei prossimi tre-quattro mesi». A detta sua, l’impatto delle manovre delle autorità può dirsi positivo. [Modificato da (sylvestro) 19/06/2012 07:05] |

| |

| 28/06/2012 14:53 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

OSSERVATORIO FIMAA

In Slovenia anche il mercato immobiliare denuncia una forte sofferenza

di Francesco Fain

Ma qual è la situazione del comparto edile in Slovenia? Un breve ma significativo punto della situazione lo fornisce la Federazione italiana mediatori ed agenti d’affari, meglio nota con l’acronimo di Fimaa. Alla pagina 55 dell’«Osservatorio 2012 del mercato immobiliare» c’è un capitolo riguardante proprio la situazione al di là del confine che non c’è più. «Come membro dell’Eurozona - evidenzia la Fimaa - il mercato immobiliare della Slovenia sta soffrendo anch’egli della crisi economica. Ci sono buone possibilità di investimento, soprattutto nelle zone turistiche. I prezzi sono più bassi che in Croazia o in Austria e il settore turistico tiene meglio di quello residenziale. Le quotazioni dovrebbero rimanere stabili per tutto il 2012, con buoni valori di rendimento nelle locazioni».

Il settore ha assistito ad un calo del numero di progetti dall’inizio della crescita economica 2009, nel 2010 i lavori sono stati pari al 19% in meno rispetto all’anno precedente. Le previsioni per il prossimo trimestre sono negative. Un’analisi che fa il paio con quella relativa al comparto del Friuli Venezia Giulia illustrata durante gli “Stati generali delle costruzioni” svoltosi alla fiera di Pordenone nel maggio scorso. «Nell’ambito complessivo delle costruzioni nei tre anni del periodo 2009-2011 il saldo tra le assunzioni e le cessazioni nelle costruzioni del Friuli Venezia Giulia ha avuto segno negativo - si legge nelle documentazioni -. Alla riduzione delle perdite registrata nel 2010 (-521 posti di lavoro nel 2010 contro il -1.000 del 2009) si contrappone un nuovo inasprimento nel 2011, pari a -991 posti di lavoro. Allo stesso tempi diminuisce il numero di assunzioni, con un tasso annuo pari al -11% rispetto, ad esempio, a una crescita contenuta sia in Veneto (+1%) sia in Emilia Romagna (+3%)».

Il futuro? Gli imprenditori del settore prevedono variazioni della produzione e del fatturato negative per il prossimo trimestre e oltre il 40% variazioni attorno allo zero. Le aspettative dei costi di produzione sono invece orientate ad una crescita sostenuta nel breve termine: è infatti consistente il saldo positivo tra coloro che hanno espresso crescita per i prossimi mesi rispetto a chi prevede ancora variazioni negative.

©RIPRODUZIONE RISERVATA |

| |

| 28/06/2012 17:20 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

La bolla immobiliare in Norvegia mette (altre) ansie all’Europa

Fabrizio Goria

In Norvegia i prezzi delle case continuano a salire. Dal 2008 a oggi l’impennata è stata del 30 per cento. E la Federal Reserve di San Francisco mette in guardia Oslo, rimarcando che i rischi possono destabilizzare il sistema bancario norvegese. Ma dalla Norges bank, la banca centrale nazionale, si dicono più preoccupati dalla situazione dell’eurozona, che potrebbe contagiare il Paese. Intanto, sempre più capitali volano verso i fiordi.

ECONOMIA

27 giugno 2012 - 16:37

In Norvegia ci sono le condizioni di una bolla immobiliare. A dirlo, senza troppi giri di parole, è la Federal Reserve di San Francisco. Analizzando i prezzi delle abitazioni in Norvegia e Stati Uniti, è risultato evidente a Marius Jurgilas e Kevin J. Lansing, economisti della banca centrale americana, lo squilibrio che sta vivendo il mercato immobiliare norvegese. La curva dei prezzi (il grafico è in calce all’articolo, ndr) è quasi a senso unico. Dal 2008 a oggi i prezzi sono aumentati di circa 30 punti percentuali, mentre in maggio l’incremento è stato del 7% su base annua. A oggi, escludendo la contrazione in seguito alla crisi dei mutui subprime americani, non ci sono state flessioni negli ultimi dieci anni. Un altro rischio per l’Europa? Forse no, come afferma Matt O’Brien su The Atlantic. Ma il pericolo, rimarca la stessa banca centrale norvegese, esiste.

La paura di un collasso dell’euro ha fatto dirottare gli investimenti di diversi Paesi proprio verso la Norvegia. E questi, in buona parte, sono finiti negli immobili. È questo il sunto della ricerca che la Fed di San Francisco ha condotto sul mercato immobiliare norvegese, che da anni sta registrando un’impennata dei prezzi che ricorda da vicino l’andamento che ha avuto il mercato statunitense prima del 2007. «La fuga dei capitali europei verso i cosiddetti “porti sicuri” fuori dall’eurozona sta continuando», rimarca la Fed, che però non fornisce cifre. Quest’ultime sono date invece da uno studio che ha effettuato l’agenzia di rating Fitch. Prendendo in esame solo il settore dei Money market fund (Mmf), i fondi del mercato monetario, Fitch ha evidenziato che nell’ultimo anno c’è stato un incremento del 53% dell’esposizione verso la Norvegia. «Mentre tutti gli Mmf stanno limitando le risorse nell’eurozona, stanno salendo i fondi verso le nazioni esterne, con elevati surplus di bilancio», ha evidenziato Fitch. Fra queste, la prima è la Norvegia.

Sigbjørn Johnsen, ministro norvegese delle Finanze, si dice tranquillo. «È vero che i prezzi delle case sono elevati e che diversi capitali stanno arrivando dall’Europa, ma la nostra politica è sempre stata prudenziale», ha sottolineato. Anche il Fondo monetario internazionale (Fmi), nell’ultimo rapporto sul Paese, ha rimarcato che la Norvegia deve adottare politiche macroprudenziali volte a ridurre i rischi legati all’alto indebitamento delle famiglie e agli elevati prezzi delle abitazioni. «Raccomandiamo l’uso di tutte le possibilità per evitare shock economici», ha spiegato il Fmi.

A lanciare l’allarme è stata anche Norges bank, la Banca centrale norvegese, pochi mesi fa. «Il settore Real estate sta sperimentando pressioni di valore rilevante e il rischio che si sono assunte le banche del sistema non devono essere sottovalutati», spiegavano l’economista Artashes Karapetyan. L’esposizione degli istituti di credito norvegesi verso il settore immobiliare, secondo Karapetyan, ammonta a circa 120 miliardi di euro, circa 901,8 miliardi di corone. Per gli economisti della banca centrale la forza patrimoniale delle banche del Paese è sufficiente a evitare qualsiasi shock.

La Norges bank non è la sola ad aver messo in guardia le banche norvegesi sulla situazione degli immobili. Anche la Finanstilsynet, l’authority di vigilanza finanziaria del Paese, ha spiegato nel suo rapporto annuale sui rischi del sistema che esiste un problema legato al prezzo, in costante salita, delle case. «I rischi presi dalle entità finanziarie norvegesi in merito al settore immobiliare sono molto elevati e raccomandiamo l’uso di stress test per verificare le resistenza patrimoniale dei singoli soggetti», ha scritto la Finanstilsynet. Sono poi arrivate le prove di solidità della European banking authority (Eba) di circa un anno, le prime a cui ha partecipato DNB Bank, il principale operatore finanziario del Paese. Tutto è andato liscio, ma nelle scorse settimane Ingvild Svendsen, direttore del dipartimento di vigilanza macroprudenziale di Norges bank, ha di nuovo posto l’attenzione dei banchieri norvegesi sulla situazione immobiliare. «Stiamo osservando una dinamica dei prezzi degli immobili che non ha paragoni nella nostra storia», ha detto Svendsen, rimarcando che la Norges bank è pronta a «ogni soluzione» per evitare squilibri macroeconomici nel Paese.

A calmare gli animi ci ha pensato Øystein Olsen, il governatore della Norges bank, durante l’ultima decisione sui tassi d’interesse, lasciati invariati all’1,50 per cento. «Stiamo monitorando la situazione e l’esempio statunitense è utile», ha rimarcato. E Olsen non ha evitato di lanciare una frecciata all’eurozona: «I maggiori problemi per la Norvegia arrivano proprio dai nostri vicini, dalla zona euro. Per fortuna siamo pronti a qualsiasi caso, anche quelli più estremi». Sarà il Consiglio europeo che inizia domani a dare un’idea di quanto dovrà preoccuparsi la Norvegia.

fabrizio.goria@linkiesta.it

Twitter: @FGoria

Leggi il resto: www.linkiesta.it/norvegia-bolla-immobiliare#ixzz1z6Me7NGT |

| |

| 29/06/2012 08:25 |

|

| | | Post: 7.647 | Sesso: Maschile | Utente semplice | Castellina in Chianti | | OFFLINE |

|

click per ingrandire

|

| |

|

|

|

|